Retailers upgrading their payments experience and fraud prevention capabilities are increasingly seeking outside expertise in their innovation journeys, going for “buy” rather than “build” in digital systems.

Analyzing results from the study “Retail Payments Innovation Year in Review: How Real-Time Payments Drive the In-Store Customer Journey,” a PYMNTS and ACI Worldwide collaboration, we find that just over half (51%) of U.S. and 63% of U.K. retailers say they’ll use third-party technology partners for innovative tech, with 1 in 3 saying efforts will combine both.

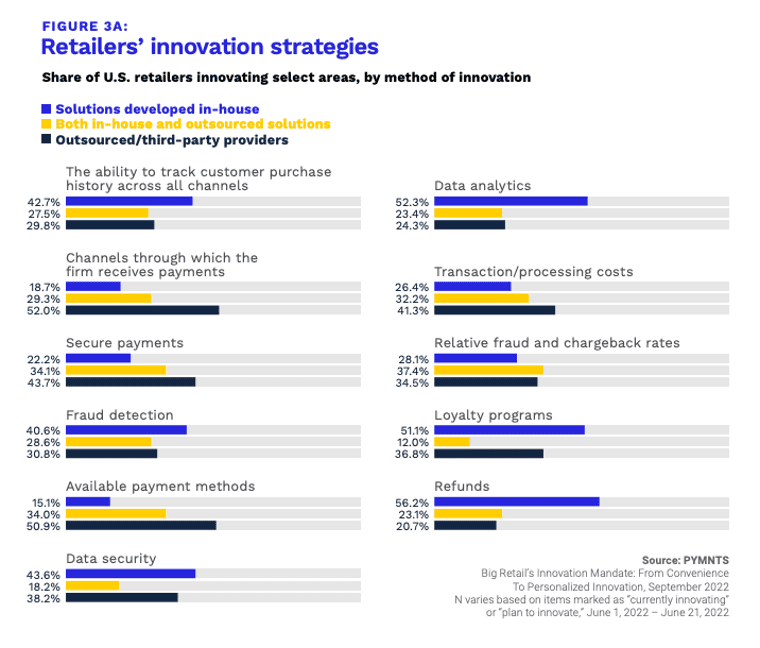

The use of third parties underscores the growing complexity of systems needed for retailers to create the digital experiences that are most in demand by consumers in 2023. We found that 57% of non-grocery retailers plan to outsource payment method innovation, for example.

More convenience and better customer experience are driving retailers to seek third-party expertise as they seek scalability and proven functionality without the time and cost of developing these systems in-house.

As the study notes, “75% of all respondents cited improved customer experience as the reason to implement digital in-store tools, 31% said it was the most important reason. Another 63% cited convenience as their motivation to use these tools, with 13% saying it was the most important draw.”

Though 2023 is a challenging time to be making major system investments, retailers’ primary concern is that not having proven capabilities can put them behind the 8-ball competitively.

Get the study: Retail Payments Innovation Year in Review: How Real-Time Payments Drive the In-Store Customer Journey

PYMNTS concluded that “Retailers that invest in more digital in-store features believe that customers are less likely to switch to another merchant, while those offering the fewest digital tools think consumers will more likely switch to another merchant because of the lack of digital features. More than three-quarters of retailers believe that consumers would be very or extremely likely to switch merchants because retailers are not providing capabilities such as mobile apps, barcode and QR code scanner apps, or alternative payment methods in-store.”

An example of the third-party systems expected to be sought this year by merchants is ACI Instant Pay. Introduced in January, ACI Instant Pay is getting the jump on the Federal Reserve’s FedNow instant payments system being launched later this year.

In an interview with PYMNTS, Basant Singh, head of merchant payments at ACI Worldwide, said, “Settlement for the merchant will happen instantly. The benefit to the consumer is that there is another option for them, especially for the newer demographics like Gen Z and younger generations. They are very keen to adopt this kind of instant payment. This is the right payment option for them.”

There are no interchange fees for use of ACI Instant Pay. Merchants pay a flat fee for the instant payments functionality, which is also expected to reduce chargebacks.

See also: ACI Worldwide Debuts ‘Instant Pay’ Ahead of FedNow Launch

Not all upgrades will be outsourced. The research found that non-grocery retailers plan to develop loyalty programs, refund solutions and data analytics innovations in-house more than other capabilities.

However, in addition to payment methods, merchants will be relying more heavily on third parties for help in data security and fraud detection from companies with deep expertise in these areas.

Per the study, “Approximately 40% of both U.S. and U.K. retailers reported currently innovating around data security. A similar share of U.K. retailers (39%) plan to innovate in the next 12 months. More than half of U.K. retailers are already engaged in fraud detection innovation, and 18% plan to innovate. In the U.S., 37% of retailers have introduced these innovations and 37% have innovation plans.”

For all PYMNTS retail coverage, subscribe to the daily Retail Newsletter.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More